What is Small Group Insurance?

In most states, the term “small group” applies to groups of 2 to 50 employees. And in California, Colorado, New York, and Vermont, it includes groups with up to 100 employees. Businesses that fall into the small group category all have the same coverage options available in the small group market, and the rules in terms of pricing and coverage availability are the same regardless of whether you have two employees or 42.

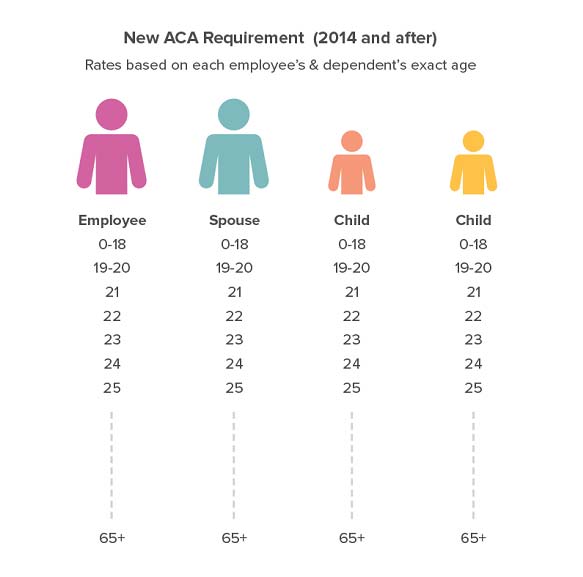

Often, small group insurance is far more affordable than the equivalent individual policy. This is because the insurance company can negotiate better rates with hospitals, clinicians and other services. There are also legal limits set for premiums – for example premiums for older employees cannot be more than three times those for younger employees.

A question we get a lot from people searching for affordable group health plans is how the Affordable Care Act (Obamacare) has changed group health insurance in California. They want to know:

- Who classifies as a “small business employer.”

- What determines the “premium?”

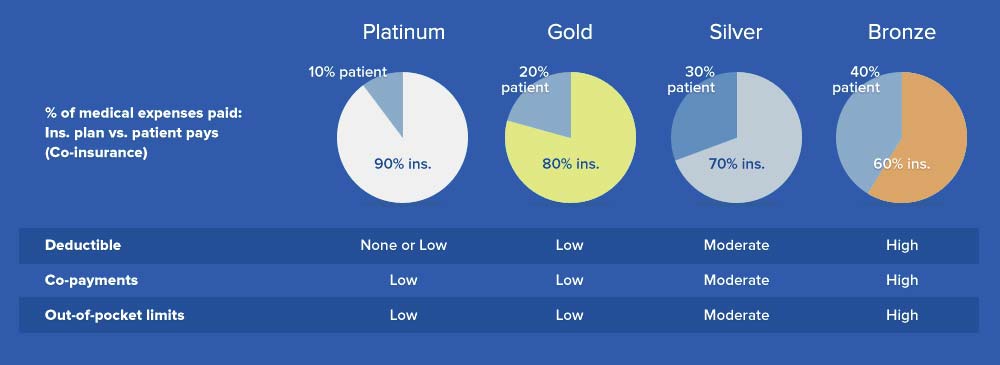

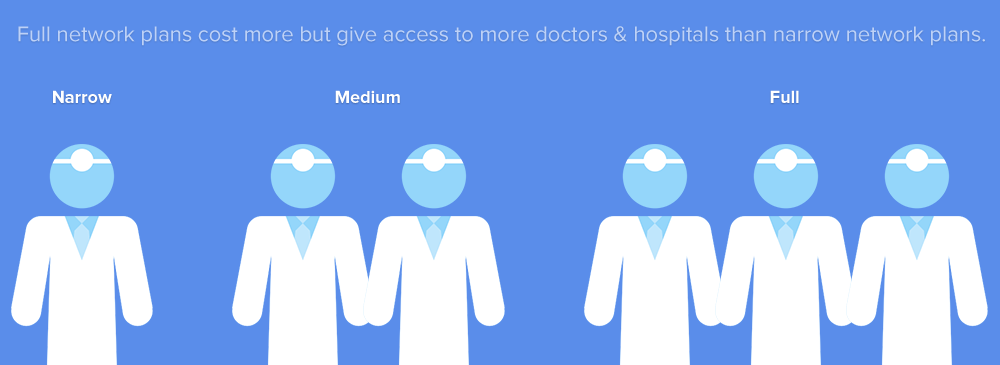

- How can I compare plans? (cost of doctor visits, in-hospital services, prescriptions).

- What sort of tax benefits does group medical insurance offer employers and employees?

To answer common questions about the ACA and help demystify group health insurance in general, we’ve created a few easy-to-digest graphics to break things down. You’ll also find a list of resources covering California group medical insurance and tips for selecting the right plan for your employee health benefits.

Running a business is hard enough without navigating the ins and outs of group health insurance. We’re expert benefit advisors with decades of experience and we’re ready to help at no additional charge or fees.

Group Insurance Questionnaire

Fill out the form below to get started.